Effective immediately Disqualified students who are authorized by the instructor to take their class through Open University shall be allowed to do so. Courses taken through Open University can be used to raise the GPA, for Grade Replacement or to complete a course that is offered only once per year.This is not a matter of not allowing disqualified students from taking seats that registered students want. When a student registers for a class through Open University, s/he sits in the same classroom, hears the same lectures, and does the same work as the regularly registered students. S/he just pays more.

Campus policy specifically prohibits matriculated students with continuing student status from taking classes through Open University. However, since Disqualified students are neither matriculated nor do they have continuing student status, there is no basis in policy for preventing them from taking courses through Open University. If you have any question please contact the Office of Undergraduate Studies.

Tuesday, June 29, 2010

From the business office

I recently received this email "on behalf of our Dean of Undergraduate Studies."

Monday, June 28, 2010

Saturday, June 26, 2010

Friday, June 25, 2010

Pleasure and pain

Paul Bloom's new book (How Pleasure Works: The New Science of Why We Like What We Like) is about what makes us take pleasure in things. As a NYTimes review explains, Bloom's theory is that pleasure is derived from our sense that things have an "essential nature" and that it's the essential nature that shapes our pleasure—or lack thereof.

Bloom’s ideas go against the traditional view of pleasure as purely sensory: that is, that we get pleasure from food because of how it tastes, from music because of how it sounds, from art because of how it looks. The sensory explanation is only partially true, he writes. “Pleasure is affected by deeper factors, including what the person thinks about the true essence of what he or she is getting pleasure from.” When we pay good money for tape measures that famous people have touched—in 1996 someone paid $48,875 for a tape measure once owned by John F. Kennedy—or treasure our children’s clumsy kindergarten art, it is because we believe that something about the person’s essence exists in the object itself.That may or may not be a useful explanation. What Bloom doesn't attempt to do is to explain what pleasure is. Why is it that we describe certain neurological events as pleasurable and others as painful? That to me is the real mystery.

The music animation machine

I saw this once before with a Bach piece. Here it is with Debussy. It's terrific. (Too bad the sound quality isn't very good. Or is it my computer?)

Here's the website.

Here's the website.

Why is a cheap Renminbi bad?

Paul Krugman has a column about the evils of the undervalued Renminbi. I'm afraid I don't get it. Here is the comment I left.

Let's say we discover a civilization on Mars. Let's suppose that civilization produces clothes, DVD players, and other items we value. Let's say that this civilization wants nothing more than to make us happy. It does that by giving away all the stuff it produces. Why is that bad for us?

Isn't that the extreme case of China? How can selling us stuff for less than it's worth be bad for us? I can think of three possible arguments.

1. In producing the stuff China is selling us it uses too much of the world's supply of raw materials. Since it is giving us the final product at an unnaturally low price it is essentially putting those raw materials to use in wasteful ways. If we were forced to pay full price for those raw materials perhaps we would use them more wisely.

But I doubt that's the fundamental problem. Aren't we more concerned that China is giving us under-priced labor than under-priced materials.

2. By fulfilling our needs and desires China is depressing our economy because once those needs and desires are met we don't want anything more. Hence no (or reduced) internal demand.

But that doesn't convince me. If we can't find anything else to want once we get all our superficial needs and desires satisfied, we are not very imaginative. It should work the other way. Once our simple needs and desires are satisfied that leaves room for more sophisticated needs and desires. After all, we get our food for very little. That's not bad; it's good. It leaves room for us to want things other than food. So why is it bad to get other things cheaply?

3. By accumulating dollars, China is putting itself in a position to buy our productive assets. When it does that we will be working for them.

I suppose that's a real problem. But that doesn't seem to be what people are worrying about.

So as I said, I'm confused and would appreciate a further explanation.

Thursday, June 24, 2010

Flight Tracker

The FlightTracker website tracks any US flights and some non-US flights. Just give it the airline and flight number or the departure and destination cities, and it will track the flight showing you a map (using Google maps) with the position of airplane. It also shows the scheduled departure and arrival times.

I know all this because my wife is coming home from the East Coast today. Her flight (UA 29) from JFK was delayed 1 1/2 hours taking off. She is now over West Virginia and is scheduled to arrive here at about 1:30 Friday morning.

I know all this because my wife is coming home from the East Coast today. Her flight (UA 29) from JFK was delayed 1 1/2 hours taking off. She is now over West Virginia and is scheduled to arrive here at about 1:30 Friday morning.

Tuesday, June 22, 2010

Does the Holder v. Humanitarian Law Project decision make the U.S. a Fascist Police-State?

Tough words, but read Gonzalo Lira's guest post in Naked Capitalism. Here's the summary paragraph.

[In its decision in Holder v. Humanitarian Law Project the Supreme Court decided that the] U.S. government can decide unilaterally who is a terrorist organization and who is not. Anyone speaking to such a designated terrorist group is “providing material support” to the terrorists—and is therefore subject to prosecution at the discretion of the U.S. government.

Should auto dealers be waived from consumer protection reform?

From Join Campaign for America's Future.

Earlier today, the House members of the House-Senate conference committee crafting the final version of financial reform voted to create a loophole exempting auto dealers from any new consumer protection rules.

We cannot let this stand, and we have no time to lose.

Join Campaign for America's Future and CREDO in telling Rep. Barney Frank and Sen. Christopher Dodd: No consumer protection loopholes for auto dealers!

While a lot of attention has been paid to banks, we can't lose sight of car dealers, who are responsible for some of the most abusive financing deals.

In fact, abusive deals by auto dealers rank top among the complaints filed each year with state consumer protection agencies. …

Tell the leaders of the House-Senate conference committee, Rep. Barney Frank and Sen. Chris Dodd, that all consumers should be protected from shady financial deals.

We can't let Congress sell out consumers by giving a free pass to car dealers in the final bill.

Everyone should play by the same rules when it comes to making loans. Banks and credit unions aren't exempted from the new rules, and car dealers shouldn't be either.

With high-pressure tactics, dealers often lock buyers into higher-interest loans than they'd qualify for elsewhere. Then they turn around and sell the note to finance companies, who give the dealer a kickback for steering customers into high-interest loans and overpriced add-ons.

Bad auto loans are such a problem for our soldiers that the Pentagon has come out against the auto-dealer exemption. Even General David Petraeus' wife, Holly, who is working to help military families avoid financial scams, is fighting this rotten deal!

The Neuroscience of Distance and Desire

An article in Scientific American says that things we want appear closer (and more easily attainable) than things we don't want.

For example, [experimental subjects] who had just eaten pretzels perceived a water bottle as significantly closer to them relative to participants who had just drank as much water as they wanted.This echos the idea that we have evolved to be optimistic. We are motivated

to pursue those goals that are particularly desirable, and encourage us to not pursue those goals that might be particularly difficult to attain. The logic here is simply that energy is a limited resource, and over evolutionary time the individuals who have been most successful have been those who directed their energy towards goals that would either benefit them the most or that would not come at too high a risk.There is other research that says that depressed people—who tend to have reduced desire for anything—are typically more accurate in estimating the probabilities that desirable things will happen. The rest of the world tends to be too optimistic.

The closer an object appears, the more obtainable it seems. The more obtainable it seems, the more likely we are to go for it. Likewise, the more challenging a goal appears … the more distant it will seem. … That chasm over there? Impossible to jump across. How about that growling bear? It’s impossible to physically subdue. There would have been goals that were impossible or, at least, very difficult or unlikely for an individual to achieve, and having the perceptual system guide us in the right direction (e.g. by making the chasm look wider than it actually is, and the bear perhaps a bit larger and meaner) would have been extremely important.

Three dropouts

Here's a great story about the lives of three people who dropped out of the Harvard College class of 1969. They have all made good lives for themselves while essentially remaining drop-outs.

Monday, June 21, 2010

How to impress the bond markets

Dean Baker has three great ways to reduce the deficit. Why don't we hear any of the deficit hawks talking about any of them?

For item number 1: how about a financial speculation tax? Wouldn't the bond markets be impressed by seeing Congress crack down on the Wall Street hot shots whose recklessness helped fuelled the housing bubble? That one would show real courage given the power of Goldman Sachs-Citigroup gang.

As a second item, Congress could go after the pharmaceutical industry. By 2020 we are projected to be spending almost $500bn a year on prescription drugs. We pay close to twice as much for our drugs as people in other wealthy countries and about 10 times as much as the drugs would cost if they could be sold in competitive market without government patent monopolies.

Suppose Congress decided to pay for the clinical testing of drugs directly and then allowed all new drugs to be sold as generics. This could save taxpayers hundreds of billions of dollars a year. Wouldn't the bond markets be impressed by seeing Congress stand up to the pharmaceutical industry?

As a third item, suppose Congress revisited plans for a public insurance option. The Congressional Budget Office projected that this would save over $100bn by 2020 and certainly much more in future decades. Wouldn't the bond markets be impressed if Congress stood up to the insurance industry?

These are three clear ways in which Congress can take big steps towards reducing long-term budget deficits by standing up to powerful interest groups. In each case Congress would be reducing the deficit in ways that would likely make most people better off, not worse off. If bringing the long-term deficit into line is the issue, all three of these measures should be at the top of everyone's list.

Remarkably, the leading budget hawks never discuss these measures when they push their deficit-cutting agenda. Somehow we are supposed to believe that cutting social security will do the trick with the markets, even though this will hurt tens of millions of people who actually need the money.

China is not really monitarist

Dave Rosenberg talks a bit about China's loosening of it currency control in his "Breakfast with Dave" this morning. What struck me was this.

Rosenberg thinks that at least the Canadian dollar is the place to be. (He is Canadian and writes from Toronto.)

While the U.S. still has a huge trade deficit with China, it is almost alone in this regard because Japan enjoys a $45 billion bilateral surplus with China; South Korea has a $59 billion surplus and Brazil too, at $14 billion. In fact, outside of the U.S., China is running a deficit with the G20.So it's not really the case that China is undercharging for its goods. It's more like we just aren't competitive. That suggests that the dollar should be devalued. But with the Euro and perhaps the Pound also being devalued, what's left to devalue against? The Yen? The Swiss Frank. The Australian and Canadian dollars? The Brazilian Real? The Indian Rupee? The Swedish Krona?

Rosenberg thinks that at least the Canadian dollar is the place to be. (He is Canadian and writes from Toronto.)

It is difficult to see … the Canadian dollar failing to remain in what looks to be a long-term bull market.That suggests that a safe and smart place to put one's savings is in Canadian government bonds. Earn interest and get capital appreciation at the same time.

Sunday, June 20, 2010

A golden age of visuals

I just subscripbed to yet another visual blog. There seem to be more and more sources that focus on making information available in a form that's easily and quickly digestable. All-in-all, I think that's a good thing. Here is my current list.

Besides these, there is all sorts of economic data. For example, The NYFed regularly publishes an enormous number of data series. So does the Dept. of Commerce's Bureau of Economic Analysis.

EconomPicDataI had expected to find more in my list. (I excluded all the stock market charting sites.) But that's all there were.

FlowingData

Gapminder

Information is Beautiful

Strange Maps

VisualEconomics

VisualScience

Besides these, there is all sorts of economic data. For example, The NYFed regularly publishes an enormous number of data series. So does the Dept. of Commerce's Bureau of Economic Analysis.

The ABCDEs of melanoma skin cancer

Be careful of the sun.

From http://myhealth.ucsd.edu/

From http://myhealth.ucsd.edu/

Source: NCI Visuals Online. Skin Cancer Foundation.

The ABCDEs of melanoma skin cancer are:

- Asymmetry. One half doesn't match the appearance of the other half.

- Border irregularity. The edges are ragged, notched, or blurred.

- Color. The color (pigmentation) is not uniform. Shades of tan, brown, and black are present. Dashes of red, white, and blue add to a mottled appearance.

- Diameter. The size of the mole is greater than 1/4 inch (6 mm), about the size of a pencil eraser. Any growth of a mole should be evaluated.

- Evolution (not shown in the picture). There is a change in the size, shape, symptoms (such as itching or tenderness), surface (especially bleeding), or color of a mole.

Friday, June 18, 2010

A message?

From USATODAY.com

Before:

During:

I couldn't resist.

Monroe [Ohio] fire officials set damage at $700,000 after lightning struck and burned down a 62-foot-high Jesus Christ statueThe statue is known as Touchdown Jesus because the arms were raised like a referee signaling a touchdown.

Before:

During:

I couldn't resist.

Fiscal Fantasies

From Paul Krugman's blog. Many of the references are links in the original.

It’s really amazing to see how quickly the notion that contractionary fiscal policy is actually expansionary is spreading. As I noted yesterday, the Panglossian view has now become official doctrine at the ECB.

So what does this view rest on? Partly on vague ideas about credibility and confidence; but largely on the supposed lessons of experience, of countries that saw economic expansion after major austerity programs.

Yet if you look at these cases, every one turns out to involve key elements that make it useless as a precedent for our current situation.

Here’s a list of fiscal turnarounds, which are supposed to serve as role models. What can we say about them?

Canada 1994-1998: Fiscal contraction took place as a strong recovery was already underway, as exports were booming, and as the Bank of Canada was cutting interest rates. As Stephen Gordon explains, all of this means that the experience offers few lessons for policy when the whole world is depressed and interest rates are already as low as they can go.

Denmark 1982-86: Yes, private spending rose — mainly thanks to a 10-percentage-point drop in long-term interest rates, hard to manage when rates in major economies are currently 2-3 percent.

Finland 1992-2000: Yes, you can have sharp fiscal contraction with an expanding economy if you also see a swing toward current account surplus of more than 12 percent of GDP. So if everyone in the world can move into massive trade surplus, we’ll all be fine.

Ireland, 1987-89: Been there, done that. Let’s all devalue! Also, an interest rate story something like Denmark’s.

Sweden, 1992-2000: Again, a large swing toward trade surplus.

So every one of these stories says that you can have fiscal contraction without depressing the economy IF the depressing effects are offset by huge moves into trade surplus and/or sharp declines in interest rates. Since the world as a whole can’t move into surplus, and since major economies already have very low interest rates, none of this is relevant to our current situation.

Yet these cases are being cited as reasons not to worry as austerity becomes the rule.

You know what? I’m worried.

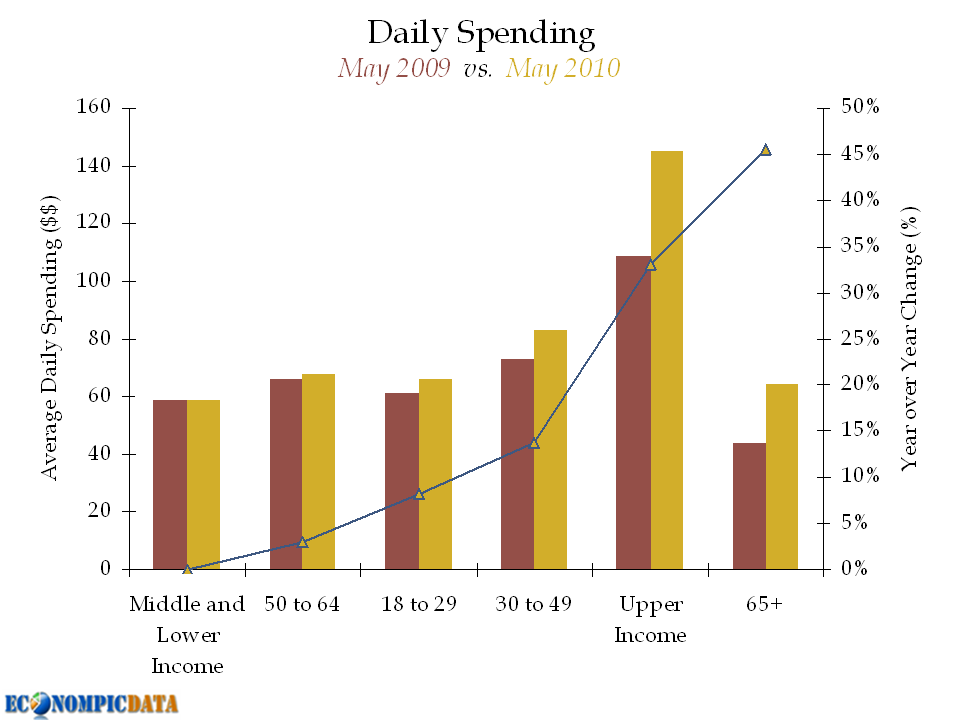

Consumers are spending more

And richer and older consumers are spending even more. (From Econompicdata.)

Thursday, June 17, 2010

I.B.M.'s Supercomputer to Challenge 'Jeopardy!' Champions

Nice NYTimes.com article on Watson, IBM's question answering super-computer.

The great shift in artificial intelligence began in the last 10 years, when computer scientists began using statistics to analyze huge piles of documents, like books and news stories. They wrote algorithms that could take any subject and automatically learn what types of words are, statistically speaking, most (and least) associated with it. Using this method, you could put hundreds of articles and books and movie reviews discussing Sherlock Holmes into the computer, and it would calculate that the words “deerstalker hat” and “Professor Moriarty” and “opium” are frequently correlated with one another, but not with, say, the Super Bowl. So at that point you could present the computer with a question that didn’t mention Sherlock Holmes by name, but if the machine detected certain associated words, it could conclude that Holmes was the probable subject — and it could also identify hundreds of other concepts and words that weren’t present but that were likely to be related to Holmes, like “Baker Street” and “chemistry.”

In theory, this sort of statistical computation has been possible for decades, but it was impractical. Computers weren’t fast enough, memory wasn’t expansive enough and in any case there was no easy way to put millions of documents into a computer. All that changed in the early ’00s. Computer power became drastically cheaper, and the amount of online text exploded as millions of people wrote blogs and wikis about anything and everything; news organizations and academic journals also began putting all their works in digital format. What’s more, question-answering experts spent the previous couple of decades creating several linguistic tools that helped computers puzzle through language — like rhyming dictionaries, bulky synonym finders and “classifiers” that recognized the parts of speech.

Machine trading

From The Atlantic.

On the third floor of Citigroup’s Manhattan headquarters, at the far end of a trading floor overlooking the Hudson River, Young Kang, Citi’s global head of algorithmic products, leans over a terminal and monitors the progress of a canny and powerful beast named Dagger. Bred and trained in secret by Citi’s financial engineers, Dagger can stalk through more than 20 markets, public and otherwise—hunting for anomalies, buying and selling, prowling through mountains of historical data—all at the behest of Citi’s clients. Amid the trading-floor din, Dagger fulfills its duties in flickering silence, with a speed and acuity no human can match.

“It’s self-learning,” Kang says. “The numbers keep updating, the strategy keeps adjusting itself. It gets smarter.”

And it makes a lot of money. Algorithms like Dagger can exploit the smallest inefficiencies in the market. They can parse trades in millionths of a second. Some species can detect other algos embarking on predictable trading strategies, and ruthlessly adjust their techniques. They’re growing ever more complex, subtle, and sophisticated. And as they become more popular, they’re creating some serious headaches for regulators.

By some estimates, algorithms now trigger 70 percent of all trades in U.S. equities. The speed and volume of everyday trading have propelled the market into a new and esoteric dimension, and rendered traders in the pits largely obsolete. Average daily share volume on the New York Stock Exchange increased by 181 percent between 2005 and 2009, while the time required to execute a trade on its electronic systems dropped to 650 microseconds.

Such changes have a lot of people worried, including the Securities and Exchange Commission. It released a wide-ranging paper earlier this year seeking suggestions on how to restructure the entire equity market, and created a Division of Risk, Strategy, and Financial Innovation in part to help monitor new technologies. A market collapse in early May—in which automated-trading systems exacerbated a sell-off that drove the Dow down more than 900 points in less than an hour, before it quickly recovered—gave two worries new public salience: that the proprietors of these algos may not be in full control of their creations, and that the strategies they pursue are, in some cases, fundamentally warping the financial markets.

In January, the NYSE fined Credit Suisse $150,000 for “failing to adequately supervise the development, deployment, and operation of a proprietary algorithm.” The fine was a pittance, but more troubling was that the bank didn’t even know that its malfunctioning algo (which sent hundreds of thousands of cancel-and-replace requests for orders that hadn’t been made) had crippled some of the NYSE’s trading stations until regulators called them the next day. This spring, a newsletter from the Federal Reserve Bank of Chicago warned: “Although algorithmic trading errors have occurred, we likely have not yet seen the full breadth, magnitude, and speed with which they can be generated. Furthermore, many such errors may be hidden from public view.”

Bernard Donefer, a finance professor at Baruch College and the author of a study in the most recent Journal of Trading called “Algos Gone Wild,” contends that the speed of these equations, and their ability to reach so many markets simultaneously, could turn even a minor coding error into a spiraling disaster. “Another 1987,” he told me, referring to the epic crash caused in part by simpler automated-trading schemes. This view puts Donefer in the minority in the financial community, which tends to have more faith in firms’ internal risk controls. But he thinks that without better regulation, more algo-gone-wild scenarios are inevitable. He notes that while controls at big firms, like Citi, are generally exemplary, second- and third-tier firms present a graver risk.

The SEC wants to hire a lot more staffers, both for its new risk division and for its trading division, and it is considering new methods of tracking algorithmic trades; Donefer and others have suggested a tagging system for the biggest traders, which the SEC says is on the table. The commission also may soon outlaw a practice called “naked access,” in which some broker-dealers offer their clients direct access to exchanges—allowing them to potentially bypass risk controls—in pursuit of faster trading.

A more widespread worry, now getting increased attention from regulators and Congress, is a strategy known as high-frequency trading. Employers of this technique apply algorithms and other automated technology, along with real-time market data, to buy and sell so quickly (in microseconds) and in such quantities (millions of trades a day), that they engorge themselves on penny differentials in prices. These traders argue that they supply the market with needed liquidity and tighter spreads. Regulators tend to agree, for the most part; free markets have always rewarded better information, speed, and creativity. But this technology unloads on such a massive scale, and so quickly, that they fear it could feed a dangerous and self-reinforcing volatility.

At least a few high-frequency traders have learned to make a killing by detecting the more simplistic algo strategies deployed by basic pension funds and mutual funds, buying the next stock the funds plan to buy, and then selling it to them at a higher price. This may not be illegal, but it’s almost certainly unfair to the funds’ investors. “It is increasingly clear that there are quite a number of high-frequency bandits in the high- frequency-trading community who pump up volume statistics, front-run investor orders, increase transaction costs, and hurt real liquidity,” David Weild, an adviser at Grant Thornton and a former vice chairman of Nasdaq, told me. *

These changes in trading technology raise a more fundamental question: If the majority of trades racing back and forth are simply lines of code swapping with other lines of code, moved by indicators obscure to even the mortal authors of the algorithms themselves, what exactly is the financial market? “The market structure’s totally changed, and it’s distorted what we do,” says Joe Saluzzi, the co-head of equities trading at Themis Trading and a vocal opponent of some high-frequency strategies. “The machine thinks for itself.”

Ignoring Maher Arar won't make his torture claims go away

Dahlia Lithwick write about an apparently outrageous torture case the Supreme Court refuses to hear.

This week the Supreme Court denied, without comment, the appeal of Maher Arar, a dual citizen of Canada and Syria who was arrested in transit through JFK airport in 2002, then shipped off to Syria and tortured for 10 months. Arar's abuse allegedly included repeated beatings with electrical cables and confinement in a cell the size of a grave. When they realized they had the wrong guy—the really, totally, and utterly innocent guy—Arar was released without charges. He was then completely exonerated of any link to terror by the Canadian government, which impaneled a commission to investigate the incident, issued a 1,000-plus-page report on the matter, held its own intelligence forces responsible for their role in the screw-up, then apologized and paid Arar $9.8 million. Whereas the U.S. government—as Glenn Greenwald observes—has never apologized, never acknowledged any wrongdoing, never held anyone responsible, and, on President Barack Obama's watch, has only redoubled its efforts to prevent Arar from having even a single day in court. …

One of the dissenters in the 2nd Circuit's fractured opinions in Arar pointed out how bizarre it is to even suggest that there is something special about torture and rendition that insulates it from any judicial scrutiny. Citing the very language of the Convention Against Torture, Judge Barrington Parker pointed out that "[n]o exceptional circumstances whatsoever, whether a state of war or a threat of war, internal political instability or any other public emergency, may be invoked as a justification of torture." Given that this is the law, he wondered, why was the majority of the panel searching high and low for some diplomatic, national security, or supersecret policy reason to defer to the other two branches of government to set the parameters of U.S. torture policy. There is no U.S. torture policy. We don't torture. So why are the courts leaving it to Congress to set its boundaries?

There are many reasons to be horrified that the courts have ended Arar's lawsuit before it could even begin, but chief among them is that the U.S. government was responsible for a year of abuse of an innocent Canadian. Having tossed out this unconscionable case, the court makes it impossible to make space for the more ambiguous ones. As David Cole, one of Arar's attorneys put it yesterday, in a piece that ought to be read in its entirety:In twenty-five years as a civil rights and human rights lawyer, I have never handled a case of more egregious abuse. US officials not only delivered Arar to Syrian security forces that they regularly accuse of systematic torture, but did everything in their power to ensure that Arar could not get to a court to challenge their actions while he was in their custody.

Wednesday, June 16, 2010

“When the sunlight strikes raindrops in the air, they act like a prism and form a rainbow.”

Discoblog reports that when a man says that sentence others (both men and women) can make a pretty good estimate of how strong he is.

So I went looking for a picture of a strong man to decorate this post. Here's what Google found for me.

So I went looking for a picture of a strong man to decorate this post. Here's what Google found for me.

Monday, June 14, 2010

Sunday, June 13, 2010

The problem of philosophy

Notre Dame publishes a regular online series of reviews of philosophical books. This one reviews Ari Hirvonen and Janne Porttikivi (eds.), Law and Evil: Philosophy, Politics, Psychoanalysis, Routledge, 2010. Bob Vallier, DePaul University, the author of the review, begins by talking about what he calls the problem of evil.

For me it raised problem of philosophy itself.

If this tempts you to look further into the book under review, here is Vallier's overall summary.

[The problem of evil] is hardly new. It is as old as philosophy itself, a discourse which begins, one story goes, with an act of spiritual freedom that allows the first philosopher to step away from the naïve comfort of the bosom of nature and ask "why?" The conditions for the possibility of evil are established with this first act of freedom, and indeed, freedom may itself be the first act of evil, in that it commits a violence against nature, violates nature by turning it into an object for scientific inquiry and for instrumental reason. The co-originarity of freedom and evil (arguably what Kant meant by "radical evil") born of our willful separation from nature (as Schelling claims) is not only a philosophical mirror of the theological story of the Fall, but also and more importantly accounts for why the problem of evil will not go away: as long as we are free, there is evil -- not simply as a possibility, but as actuality. Kant, of course, is responding to Leibniz's notion of Theodicy, itself articulated against Bayle's skeptical argument against the goodness of God. Long after Kant's response, Nietzsche, Freud, Arendt, and others will tell a different story about evil that takes us definitively beyond its metaphysical confines.Debora remarked that if freedom is inherently evil, then how can there be good. She thought this created an opening for a book on the problem of good.

For me it raised problem of philosophy itself.

If this tempts you to look further into the book under review, here is Vallier's overall summary.

On the whole, this is an interesting but uneven collection, approaching the problem of evil from three distinct but complementary discursive positions. Many of the essays are clear and insightful, but many others are highly specialized and obfuscating.Vallier especially likes the chapter by Véronique Voruz, which he says

deserves special mention for its clarity of exposition of the Freudian death drive and Lacan's interpretation of it, focusing on "Kant with Sade," and revaluing the categorical imperative as a philosophical rationalization of moral masochism. Of all the essays in the volume, this one is the most clear, accessible, and instructive, virtues that many other essays regrettably do not possess.There's quite a punch in the notion of "revaluing the categorical imperative as a philosophical rationalization of moral masochism." Is he really saying that doing good is an act of masochism? I guess that makes Debora right about the problem of good.

Nicholas Kristof - Two Men and Two Paths

From NYTimes.com

When Wes Moore won a Rhodes scholarship in 2000, The Baltimore Sun published an article about his triumph. He was the first student at Johns Hopkins to win a Rhodes in 13 years, and the first black student there ever to win the award.

At about the same time, The Sun published articles about another young African-American man, also named Wes Moore. This one was facing charges of first-degree murder for the killing of an off-duty police officer named Bruce Prothero, a father of five.

Both Wes Moores had troubled youths in blighted neighborhoods, difficulties in school, clashes with authority and unpleasant encounters with police handcuffs. But one ended up graduating Phi Beta Kappa and serving as a White House fellow, and today is a banker with many volunteer activities. The other is serving a life prison sentence without the possibility of parole.

“One of us is free and has experienced things that he never even knew to dream about as a kid,” the successful Wes Moore writes in a new book, “The Other Wes Moore. “The other will spend every day until his death behind bars. ... The chilling truth is that his story could have been mine. The tragedy is that my story could have been his.”

For me, the book is a reminder of two basic truths about poverty and race in America.

The first is that American antipoverty efforts have been disgracefully inadequate. It should be a scandal that California spends $216,000 on each child in the juvenile justice system, and only $8,000 on each child in the Oakland public schools.

Far too many Americans are caught in a whirlpool of poverty, broken families, failed schools and self-destructive behavior that is replicated generation after generation. The imprisoned Wes Moore became a grandfather last year at 33.

The writer Wes Moore offers clues from his own experience about how boys get sucked into that whirlpool.

His father, a radio and television journalist, died of a virus after a hospital emergency room — seeing only a disoriented, disheveled black man — misdiagnosed him and sent him home to get “more sleep,” Mr. Moore writes. The writer Wes grew up in a poor, drug-ravaged neighborhood of the Bronx.

His mother worked multiple jobs and scrounged to send him to Riverdale Country School, an elite prep school, but Wes felt out of place among wealthy, white students — and his black friends at home teased him for going to “that white school.” Wes skipped classes, let his grades slip, hung out with a friend who was dealing drugs, and collided with the police.

Despairing, Wes’s mother dispatched him to a military school. There he finally began to soar.

In the case of the other Wes, there were some moments when he almost escaped. His mother was earning a college degree at Johns Hopkins — which probably would have provided the family a ladder to the middle class — when Reagan-era budget cuts terminated her financial aid and forced her to drop out.

Then the criminal Wes almost found his footing with the Job Corps. There he earned his G.E.D., testing near the top of his class, and began reading at a college level. He learned carpentry skills — but afterward never found a good job and tumbled back into his old life.

Wednesday, June 09, 2010

Monday, June 07, 2010

A lesson for Helen Thomas

Helen Thomas, the longtime White House reporter and columnist announced her retirement on Monday. This column by Richard Cohen in the Washington Post comments on what led to it.

(I tried to find a nice picture of Helen Thomas. This is the best I could do.)

(I tried to find a nice picture of Helen Thomas. This is the best I could do.)

Thomas, of Lebanese ancestry and almost 90, has never been shy about her anti-Israel views, for which, as far as I'm concerned, she is wrong and to which she is entitled. Then the other day, she performed a notable public service by revealing how very little she knew. Asked if she had any comments about Israel, Thomas said, "Tell them to get the hell out of Palestine. . . . Go home. Poland. Germany. And America and everywhere else."I had never heard of the mini-holocaust or of Patton's anit-semitism.

Well, I don't know about "everywhere else," but after World War II, many Jews did attempt to "go home" to Poland. This resulted in the murder of about 1,500 of them -- killed not by Nazis but by Poles, either out of sheer ethnic hatred or fear they would lose their (stolen) homes.

The mini-Holocaust that followed the Holocaust itself is not well-known anymore, but it played an outsize role in the establishment of the state of Israel. It was the plight of Jews consigned to Displaced Persons camps in Europe that both moved and outraged President Harry Truman, who supported Jewish immigration to Palestine and, when the time came, the new state itself. Something had to be done for the Jews of Europe. They were still being murdered.

In the Polish city of Kielce, on July 4, 1946 -- more than a year after the end of the war -- rumors of a Jewish ritual murder triggered a pogrom in which 42 Jewish Holocaust survivors were killed. The Kielce murders were not, by any means, the sole example of why Jews could not "go home." When I visited the Polish city where my mother had been born, Ostroleka, I was told of a Jew who survived Auschwitz only to be murdered when he tried to reclaim his business. In much of Eastern Europe, Jews feared for their lives.

For that reason, those who had struck out for home soon returned to DP camps and the safety of -- irony of ironies -- Germany. Some of the camps were under the command of Gen. George S. Patton, a great man on the screen, a contemptible bigot in real life. In his diary, Patton confided what he thought of Jews. Others might "believe that the Displaced Person is a human being," Patton wrote, but he knew "he is not." In particular, he whispered to his diary, the Jews "are lower than animals."

The Jews, Patton felt, had to be kept under armed guard, otherwise they would flee, "spread over the country like locusts," and then have to be rounded up and some of them shot because they had "murdered and pillaged" innocent Germans. All of this is detailed by Allis and Ronald Radosh in their book "A Safe Haven."

For the surviving Jews of Eastern Europe, there was no going home -- and no staying, either. Europe was hostile to them, not in the least appalled or sorry about what had just happened. Even the American military, in the person of the hideous Patton, seemed hostile. For most of the DPs, America was also out of the question. The United States, in the grip of feverish anti-communism and already unreceptive to immigrants, maintained a tight quota. When the Jewish DPs were polled, an overwhelming majority said they wanted to go to Palestine. They knew life would be tough there, but they would be among their own people -- and relatively safe.

The Radoshes cite Branda Kalk, a Polish Jew who lost her husband to the Germans in 1942. Along with the rest of her family, she fled east to Russia, where they remained until the end of the war, when they returned to Poland. There, a pogrom wiped out what remained of her family. Kalk was shot in the eye.

"I want to go to Palestine," Kalk told members of a U.N. investigating committee. "I know the conditions there. But where in the world is it good for the Jew? Sooner or later he is made to suffer. In Palestine, at least, the Jews fight together for their life and their country."

Walt Whitman High School in Bethesda understandably canceled Thomas's commencement address. It would be wonderful, though, if Thomas could go through with it and tell the graduates what she had learned in recent days. I hardly think it would turn her into a supporter of Israel, but it might lead her to understand why so many others are.

Update

Thomas put the following statement, dated June 4, on her website.I deeply regret my comments I made last week regarding the Israelis and the Palestinians. They do not reflect my heart-felt belief that peace will come to the Middle East only when all parties recognize the need for mutual respect and tolerance. May that day come soon.

Thursday, June 03, 2010

What Pets Can Teach Us About Marriage

From Well Blog - NYTimes.comThis column summarizes a column by Suzanne B. Phillips.

Do you greet each other with excitement, overlook each other’s flaws and easily forgive bad behavior? If it’s your pet, the answer is probably yes. But your spouse? Probably not. …

Dr. Phillips suggests we can all learn how to improve our human relationships by focusing on how we interact with our pets. Among her suggestions:

Greetings: Even on bad days, we greet our pets with a happy, animated hello, and usually a pat on the head or a hug. Do you greet your spouse that way?

Holding grudges: Even when our pets annoy us by wrecking the furniture or soiling the floor, we don’t stay mad at them.

Assuming the best: When our pets make mistakes, we don’t take it personally and are quick to forgive. We give them the benefit of the doubt. Yet when our spouse does something wrong, we often react with anger and blame.

Tuesday, June 01, 2010

Robert Kuttner on Obama

From The Huffington Post.

What do the oil catastrophe and the Wall Street collapse have in common?

Three big things, I'd say.

In both cases, a powerful, politically protected industry invented something that could not easily be repaired when it broke. We seem to be entering an age when complex technologies, whether financial or physical, sometimes literally have no solutions when they go haywire in unanticipated ways. We thought this might happen with nuclear power (and it still could); but for now deepwater drilling is the bigger menace.

Secondly, in both cases the proverbial ounce of prevention was not applied. Had existing laws been enforced, and had the political process not corrupted the regulatory process, these man-made calamities didn't need to happen.

In the case of the oil disaster, which is fast becoming the worst single environmental catastrophe ever, America's long-term failure to move away from dependence on carbon fuels combined with pure short-run political capture. By now, we should have been at the point of energy conversion where high risk, mile-deep undersea wells were not used at all. But even so, this blowout would have been averted had existing laws been enforced.

It's the same story with the financial collapse. We didn't need these exotic, doomsday financial instruments. And had the regulators not been in bed with the industry, the crisis would have been headed off at any of several earlier stages.

But the worst common element is this: both crises are teachable moments that our president could be using to transform public opinion. Yet despite these gifts from the progressive gods, President Obama seems congenitally unable to rise to the occasion.

Subscribe to:

Posts (Atom)